UAV Battery Market Outlook: Endurance, Safety & Performance Optimization 2026–2035

Market Outlook

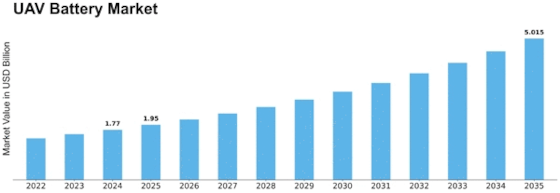

The UAV Battery Market presents a compelling growth story: from an estimated USD 1.61 billion in 2023 to about USD 5.0 billion by 2035 — a near-tripling in value and a strong ~9.9% CAGR. For battery manufacturers, this isn’t just another segment — it’s an invitation to shape the future of aerial systems.

Industry Overview

Battery manufacturers entering or expanding in the UAV space must appreciate how different this domain is from terrestrial energy storage or automotive. Key distinctions include: high weight sensitivity, extreme duty cycles, rapid power demand changes (take-off, hover, climb), mission-critical reliability, and often regulatory/airworthiness standards. Commercial drone operators demand lower cost and higher endurance; defence customers demand maximum reliability and integration with UAV systems. At the same time, as UAVs proliferate into logistics, agriculture and inspection, battery suppliers must scale cost-effectively, deliver longer cycle lives, lighter packs, faster charging or swappable modules, and integrate smart monitoring/BMS. Additionally, sustainability is increasingly important — customers and regulators alike expect lighter environmental footprints, recycling programmes, and safer chemistries.

Key Players

Manufacturers who already have experience with aerospace/defence or high-performance battery systems hold an advantage. Companies of note include:

- VARTA AG – already active in UAV-specific battery systems.

- Sion Power Corporation – bringing innovative lithium-metal technology aimed at UAVs

- Ballard Power Systems – targeting unmanned aerial systems with fuel-cell solutions built for endurance.

Practically, new entrants must evaluate whether to specialise in handheld/consumer UAV battery packs, industrial drones, or military platforms — each has very different cost/performance/qualification thresholds.

Segmentation Growth

For battery manufacturers, key segmentation insights translate into actionable opportunity zones: - Industrial/Commercial Applications: This channel offers rapid volume growth — inspection drones, logistics/delivery drones, agriculture UAVs — and creates demand for scalable, cost-effective battery systems.

- Geographic Focus: Asia-Pacific offers high growth potential given rising commercial drone adoption; North America remains lucrative for premium defence/industrial battery systems.

- Voltage/Platform Size: The jump from small consumer drones (<12 V) to medium/heavy drones (>24–48 V) signifies higher battery value per unit — more opportunity for premium systems.

- Battery Chemistry: Lithium-ion is baseline today; lithium-polymer, fuel cells and advanced chemistries will command higher margins as mission demands escalate. Manufacturers should invest in R&D for next-generation cells designed for UAV-specific applications.

Closing Thoughts

Battery manufacturers who treat the UAV segment as just “another battery application” risk missing the mark. The UAV battery market demands a nuanced understanding of aerial platform requirements, aircraft regulatory environments, rapid charging/turn-around economics, and segment-specific mission profiles. Those who align their product roadmap, manufacturing strategy and partner ecosystem accordingly will be well-positioned to reap the growth opportunity ahead.